Cash ISA Limit 2025/26: Your Complete Guide to Tax-Free Savings

Understanding the cash ISA limit is crucial for UK savers right now. The November 2025 Budget announced major changes that will affect how much you can save tax-free from April 2027. Whether you’re new to ISAs or have been saving for years, this guide explains everything you need to know.

∆∆ What Is the Cash ISA Limit?

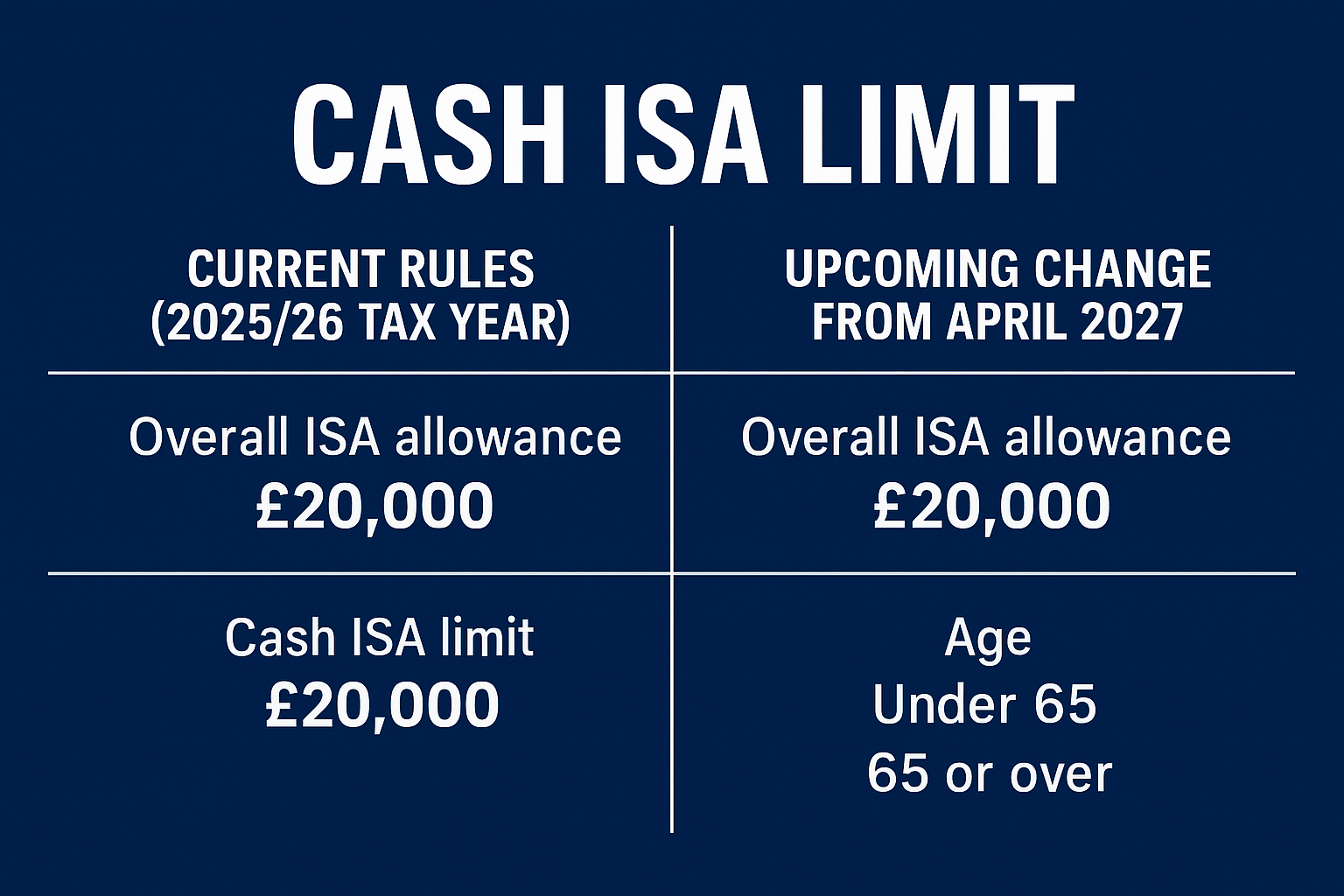

The cash ISA limit is the maximum you can deposit into a Cash ISA in a single tax year without paying tax on the interest. For 2025/26 (6 April 2025 to 5 April 2026), the cash ISA limit is £20,000.

Every penny of interest you earn is completely tax-free. No income tax. No capital gains tax. Nothing.

Here’s why this matters: basic-rate taxpayers can earn £1,000 in savings interest tax-free through their Personal Savings Allowance. With today’s rates around 4-5%, you’d hit that limit with just £22,000 in regular savings. Cash ISAs let you protect far more.

∆∆ Current Cash ISA Limit Rules (2025/26)

– Total ISA allowance: £20,000 across all ISA types

– Cash ISA limit: Up to the full £20,000 can go into Cash ISAs

– Age requirement: 18 or older

– Multiple accounts: You can open multiple Cash ISAs in the same year (since April 2024)

– Tax benefits: All interest is tax-free forever

You can split your £20,000 however you like across Cash ISAs, Stocks and Shares ISAs, Innovative Finance ISAs, and Lifetime ISAs (which have their own £4,000 cap).

Example: If you deposit £15,000 into a Cash ISA, you have £5,000 left. You could save another £5,000 in Cash ISAs, or use it for other ISA types, or split it. Your total across all ISAs cannot exceed £20,000 per tax year.

∆∆ Breaking News: Cash ISA Limit Cut to £12,000 in 2027

Chancellor Rachel Reeves confirmed on 26 November 2025 that the cash ISA limit will drop from £20,000 to £12,000 from April 2027 – but only for people under 65.

∆∆∆ Who’s Affected?

If you’re under 65:

– From 6 April 2027: Maximum £12,000 in Cash ISAs per year

– The remaining £8,000 must go into investment ISAs

– Your existing Cash ISA savings are completely unaffected

If you’re 65 or over:

– No change – you keep the full £20,000 cash ISA limit

– The government recognises that older savers need accessible, lower-risk options

∆∆∆ Why the Change?

The government wants to encourage more people to invest in stocks and shares. The UK has some of the lowest retail investment rates in the G7. By forcing the £8,000 into investments, policymakers hope to boost both individual returns and the wider economy.

However, critics call this a “stick rather than carrot” approach that limits options for people who need certainty for short-term goals.

∆∆ What Happens to Your Existing Savings?

Nothing changes with money you’ve already saved. The £12,000 limit only applies to new contributions from 6 April 2027 onwards.

Your existing Cash ISA money will:

– Remain completely tax-free

– Continue earning interest normally

– Not count towards future limits

If you’ve built up £50,000 in Cash ISAs over the years, that money stays tax-free. The £12,000 limit only affects new deposits from 2027.

∆∆ Types of Cash ISAs

∆∆∆ Easy Access Cash ISAs

Current top rates: up to 4.56%

Perfect for emergency funds and money you might need quickly. No withdrawal penalties, complete flexibility.

∆∆∆ Fixed Rate Cash ISAs

Current top rates: up to 4.3% for one-year terms

You lock money away for 1-5 years for guaranteed rates. Early withdrawal usually means penalties.

∆∆∆ Notice Cash ISAs

The middle ground between easy access and fixed. You can withdraw after giving 30-120 days’ notice. Better rates than easy access, more flexible than fixed.

∆∆∆ Regular Savings Cash ISAs

Require monthly deposits (usually £250-£300 limit). Good rates, but need consistent savings.

∆∆ Current Best Rates (November 2025)

Trading 212 offers the highest easy access rate at 4.56%. Bank of Ireland UK offers 4.11%. Best one-year fixed ISAs pay above 4.20%.

Rates are falling as the Bank of England cuts base rates. With further cuts expected, now could be a smart time to lock in current rates.

When comparing, check:

– Whether bonus rates expire

– Withdrawal rules and penalties

– Minimum deposits

– FSCS protection

∆∆ How to Maximise Your Cash ISA Limit

∆∆∆ 1. Use It or Lose It

Your allowance resets every 6 April. Unused amounts vanish forever. You can’t carry them over or save extra next year to make up for it.

With the limit dropping in 2027, you have two tax years left (2025/26 and 2026/27) to use the full £20,000 if you’re under 65. That’s £40,000 of tax-free capacity that won’t be available after April 2027.

∆∆∆ 2. Open Multiple Cash ISAs

Since April 2024, you can open multiple Cash ISAs per year. Split money between easy access (for emergencies) and fixed rate (for better returns on money you won’t need soon).

Just track your total contributions carefully – they cannot exceed £20,000.

∆∆∆ 3. Transfer Old ISAs

If you have Cash ISAs earning 1-2%, transfer them to accounts paying 4%+. This doesn’t use your current year’s allowance.

Critical: Always arrange transfers through your new provider. Never withdraw and redeposit yourself – you’ll lose the tax-free status forever.

∆∆∆ 4. Time Your Deposits

Key dates:

– 5 April 2026: Deadline for 2025/26 allowance

– 6 April 2026: Start of your last year with a £20,000 limit (if under 65)

– 5 April 2027: Final deadline for £20,000 allowance

– 6 April 2027: New £12,000 limit takes effect

If you’re expecting lump sums (inheritance, bonus, property sale), time them to maximise your allowances before the cut.

∆∆ What If You Want to Save More Than £12,000?

From 2027, if you’re under 65 and have more than £12,000 to save, you have options:

∆∆∆ Option 1: Use Investment ISAs

You’ll have £8,000 left in your ISA allowance. Consider:

– Stocks and Shares ISAs: Higher risk but historically better long-term returns

– Lifetime ISAs: If under 40, get 25% government bonus (up to £1,000 yearly) for first home or retirement

– Innovative Finance ISAs: Peer-to-peer lending (higher risk)

∆∆∆ Option 2: Regular Savings Accounts

Save outside ISAs within your Personal Savings Allowance:

– Basic-rate taxpayers: £1,000 interest tax-free

– Higher-rate taxpayers: £500 interest tax-free

– Additional-rate taxpayers: No allowance

At 4.5% rates, basic-rate taxpayers could have £22,000, earning £990 interest, still within their tax-free allowance.

∆∆∆ Option 3: Mix Both

Smart strategy for 2027:

– £12,000 in Cash ISA (emergency fund, short-term goals)

– £4,000 in Lifetime ISA (if eligible, for the government bonus)

– £4,000 in Stocks and Shares ISA (long-term growth)

– Additional savings in regular accounts within the Personal Savings Allowance

∆∆ Cash ISA Limit vs Personal Savings Allowance

Do you need a Cash ISA if you have a Personal Savings Allowance?

You probably need one if:

– Your interest exceeds £1,000 (basic-rate) or £500 (higher-rate)

– You’re a higher or additional-rate taxpayer

– You expect your savings to grow

You might not need one if:

– Your basic-rate earnings are under £1,000 interest yearly

– You have under £20,000 total savings

Currently, Cash ISAs offer higher rates than regular accounts anyway, making them worth using regardless.

∆∆ Common Mistakes to Avoid

- Missing the 5 April deadline – allowances vanish at midnight

- Withdrawing without checking if your ISA is flexible – you might lose that allowance

- Transferring money yourself instead of through your provider loses tax-free status

- Exceeding the £20,000 limit across multiple providers

- Ignoring inflation – at 3.6% (October 2025), you need rates above this for real returns

∆∆ Should You Rush Before 2027?

Don’t panic, but plan.

If you’re under 65, you have two full tax years with the £20,000 limit. That’s up to £40,000 of capacity before it drops.

However, don’t:

– Rush into poor rates just to use your allowance

– Lock money away if you might need it soon

– Save more than you can afford

– Ignore whether investing might suit some goals better

One provider saw a 49% spike in Cash ISA deposits between mid-October and mid-November 2025. Smart planning beats panic saving.

∆∆ Cash vs. Investing: What’s Right for You?

∆∆∆ Choose Cash ISAs When You:

– Need money within 3-5 years

– Are building an emergency fund (3-6 months expenses)

– Are saving for short-term goals (house deposit, car)

– Want guaranteed returns

– Are near or in retirement

– Can’t handle seeing your money fluctuate

∆∆∆ Consider Investing When You:

– Won’t need money for 5-10+ years

– Already have a cash emergency fund

– Understand investments can fall and rise

– Are you saving for retirement

– Want potential to beat inflation long-term

– Can ride out market ups and downs

Most experts recommend using both based on your different goals and timelines.

∆∆ FAQs About Cash ISA Limit

∆∆∆ What is the cash ISA limit for 2025/26?

£20,000. You can save this much in Cash ISAs during the tax year (6 April 2025 to 5 April 2026), and all interest earned is tax-free.

∆∆∆ Is the cash ISA limit changing?

Yes. From April 2027, it drops to £12,000 for people under 65. If you’re 65+, you keep the full £20,000 limit.

∆∆∆ Does the limit include interest?

No. The limit is only for deposits. If you save £20,000 and earn £800 interest, your balance can exceed £20,000 through interest without issues.

∆∆∆ Can I split my allowance between different accounts?

Yes! Since April 2024, you can open multiple Cash ISAs per year and split your £20,000 across them.

∆∆∆ What happens if I exceed the limit?

HMRC may contact you, and if you have an excess loss tax-free status, you’ll pay tax on its interest, and you might face penalties. Most providers prevent this automatically.

∆∆∆ Does transferring old ISAs use my current allowance?

No. You can transfer unlimited amounts from previous years without affecting your £20,000 limit for new contributions.

∆∆∆ Can I use all £20,000 for Cash ISAs?

Yes, currently. But from April 2027, if you’re under 65, you can only use £12,000 for cash – the remaining £8,000 must go into investment ISAs.

∆∆∆ What’s the limit for over-65s?

Over-65s keep the full £20,000 cash ISA limit even after April 2027.

∆∆∆ How does it work with the Personal Savings Allowance?

They’re separate. Personal Savings Allowance applies to regular savings interest. Cash ISA interest doesn’t count toward it and is always tax-free.

∆∆∆ Can I carry over unused allowance?

No. If you save £15,000 this year, the remaining £5,000 vanishes on 6 April. Each tax year is a fresh £20,000.

∆∆ Conclusion: Making the Most of Your Cash ISA Limit

The cash ISA limit remains one of the most powerful tools for UK savers. With the limit dropping to £12,000 for under-65s from April 2027, acting strategically matters now.

Key Takeaways

You have the £20,000 limit for 2025/26. If you’re under 65, you only have two more years before it reduces to £12,000. That’s up to £40,000 of tax-free capacity disappearing after April 2027.

Your existing savings are safe. New limits only apply to fresh contributions from April 2027. Everything already saved continues earning tax-free interest.

Current rates around 4-4.5% are competitive. Shop around and don’t settle for poor rates.

Our Recommendations

Act now. Use as much of your 2025/26 allowance as you can afford. The clock is ticking, and unused allowances vanish on 5 April.

Shop smart. With rates up to 4.56%, spending 30 minutes comparing could earn you hundreds extra yearly.

Plan by age. If you’re under 65, think about adapting to the £12,000 limit. Build cash reserves now. If you’re 65+, you keep the full limit but still prioritise good rates.

Don’t rush into investing. Keep 3-6 months’ expenses in accessible cash first. Only invest money you won’t need for 5+ years.

Transfer old ISAs. Move ISAs earning 1-2% to accounts paying 4%+. This doesn’t use your current allowance and could double returns.

Final Thoughts

The cash ISA limit is changing but not disappearing. These accounts remain valuable for protecting savings from tax.

Take action today. Review your savings, compare rates, and plan your allowance usage before changes kick in. The best financial plan is the one you implement.

Your money deserves to work harder. Don’t leave tax-free savings on the table while you still have access to the full allowance.